Featured

Table of Contents

In the ever-evolving landscape of enterprise software, mid-size companies face extraordinary difficulties driven by AI disruption, extreme competitors, slowing growth, and shifting investor needs. These companies are caught in a "big squeeze"pressured on one side by active, AI-native entrants that can replicate applications at a portion of the cost and on the other side by tech leviathans, such as Microsoft, Salesforce, and Oracle, that are putting billions into the AI arms race.

The future lies in their capability to adjust their operations and organization designs at speed, or risk being interfered with by more agile rivals. Across the business software application industry, top-line development has actually slowed considerably. Our analysis of 122 openly listed enterprise software application business listed below $10B in income shows that the percentage of high-growth companies reduced from 57% in 2023 to 39% in 2024.

While AI-native gamers have drawn in considerable recent financial investment (more than $100B in 2024 alone) and growth rates remain high, our company believe this represents only a little part of the more comprehensive business software application market. Additionally, enterprise customers are facing their own expense pressures, causing lower expansion rates and higher client churn.

As consumer demand for customized options continues to increase, the business software market has seen a surge in smaller, more nimble gamers providing specialized services, frequently at a lower cost and enabled by AI (e.g., Freshdesk from Freshworks, Zoho One from Zoho Corporation, and Representative OS from Sierra). Tech leviathans are driving consolidation through acquisitions, establishing platforms and aggressively pursuing cross-selling opportunities.

With competition building from both sides, numerous mid-size enterprise software companies are forced to reassess their method and company model. AI-driven solutions have started to make a significant impact in enterprise software application. While the most fully grown applications today are in AI-driven coding and client support (e.g. GitHub's Copilot for coding and Zendesk's Response Bot for client assistance), we are approaching a tipping point where AI will drastically enhance efficiency throughout other crucial company functions too.

Essential Lessons for B2B Success in 2026

As a result, nearly two thirds of the software company executives in our survey are concentrated on utilizing AI as a growth motorist. On the other hand, AI agents are set to disrupt the logic and discussion layer of SaaS applications. Practical examples are already appearing, such as Klarna's well-publicized decision to end its relationships with both Salesforce and Workday in favor of a suite of internal developed AI apps and smaller sized nimble suppliers.

This shift might eliminate the need for many enterprise software companies that prospered in the standard SaaS architecture. As growth continues to slow throughout both public and personal markets, financiers are putting a higher focus on profitability. Higher rates of interest are partially to blame, raising roi (ROI) targets.

In action, we have actually seen a significant pivot within the mid-sized software companies towards active expense controls and selective capital release. Business software application executives deal with a challenging job of deciding when and how to focus on running vs.

In these disruptive times, we believe the think leaders need to require both, finding a discovering towards predictable growth while driving operational rigor functional unlock funds to invest in AI.

Additionally, raised compute costs for AI agents might drive a higher expense of profits compared to conventional SaaS offerings, requiring business to reassess their cost management methods. Over the past decade, enterprise software growth has actually been centered around brand-new consumer acquisition driven by expanding item portfolios and sales teams. But in the existing environment, client acquisition is increasingly tough and costly.

This need to be enhanced by a distinct item portfolio method, value-additive AI usage cases, and innovative pricing designs. By optimizing invest across operations, enterprise software application business can open the capital to purchase high-impact developments (such as developing AI representatives) or traditional development initiatives (such as strategic collaborations). This procedure includes improving item portfolios, cutting investments in low-growth items, and utilizing AI and other automation methods to enhance front- and back-office functions.

Many business software business are pursuing acquisitions or placing themselves to be obtained by bigger players or financiers. These methods allow such business to utilize the resources and scale of bigger rivals, ensuring they remain competitive in a progressing market. This trend is echoed by the 2025 AlixPartners Interruption Index study, where growth and success leaders say they are twice as most likely to execute a deal in 2025 versus 2024.

The Future of Software Scalability

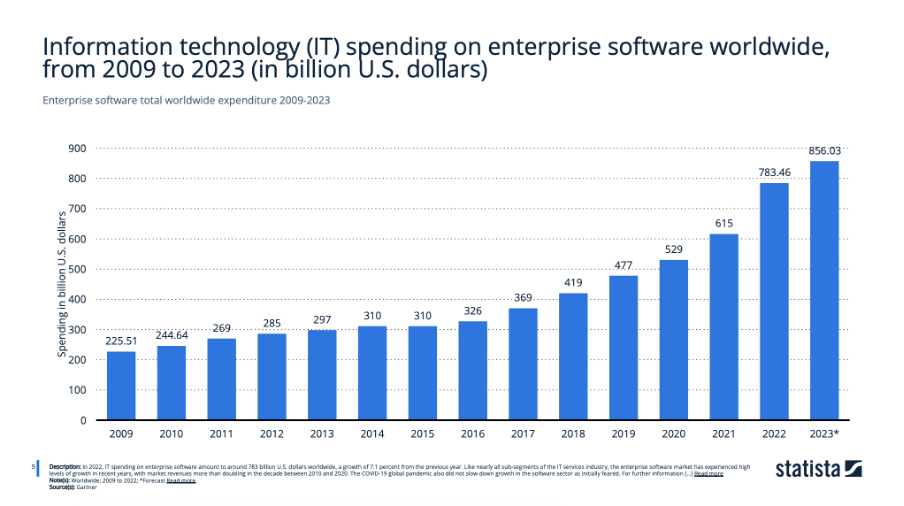

The increasing preference for automated and incorporated services is driving the growth of the marketplace. The North America business software market held a market share of over 41% in 2024. The U.S. enterprise software application market is growing substantially at a CAGR of 11.6% from 2025 to 2030. Based on implementation, the cloud sector represented the biggest market share of over 55% in 2024.

Based on end-use, the IT & Telecom sector represented the largest market share of over 20% in 2024. 2024 Market Size: USD 263.79 Billion 2030 Projected Market Size: USD 517.26 Billion CAGR (2025-2030): 12.1% North America: Biggest market in 2024 As more organizations look for structured, reliable software to reduce reliance on personnels, automate routine jobs, and reduce manual errors, the demand for enterprise software options continues to increase.

In response, market players are recognizing the growing need for sophisticated business resource planning (ERP), customer relationship management (CRM), and data analytics software, placing themselves to satisfy this need with innovative offerings. Business software is commonly used throughout different markets and sectors, including BFSI, healthcare, retail, manufacturing, federal government, and education.

As an outcome, there is a growing demand for innovative software solutions among businesses. In addition, the growing shift towards hybrid work models, accelerated by the COVID-19 pandemic, has actually considerably enhanced the adoption of business software application in markets such as health care, education, and retail.

The Importance of Software Scalability

This expanding use of business software application across markets highlights its important role in optimizing operations and enhancing efficiency in the developing digital landscape. Information safety and personal privacy are important motorists in the market, as organizations increasingly focus on the protection of sensitive details and compliance with rigid policies. With increasing issues over information breaches and cyberattacks, businesses throughout different sectors are turning to enterprise software solutions that provide robust security functions, including file encryption, multi-factor authentication, and advanced tracking tools.

This concentrate on data privacy has opened new chances for vendors using specialized software that incorporates strong security protocols while maintaining operational effectiveness. The growing trend of hybrid work environments has actually further stressed the importance of safe, remote access, making information defense a necessary consider the ongoing growth of the marketplace.

{kind=link}

Latest Posts

Securing Your Digital Platform for AI Discovery

Why Machine Learning Influences Future Search Signals

Evaluating the JavaScript Frameworks in 2026